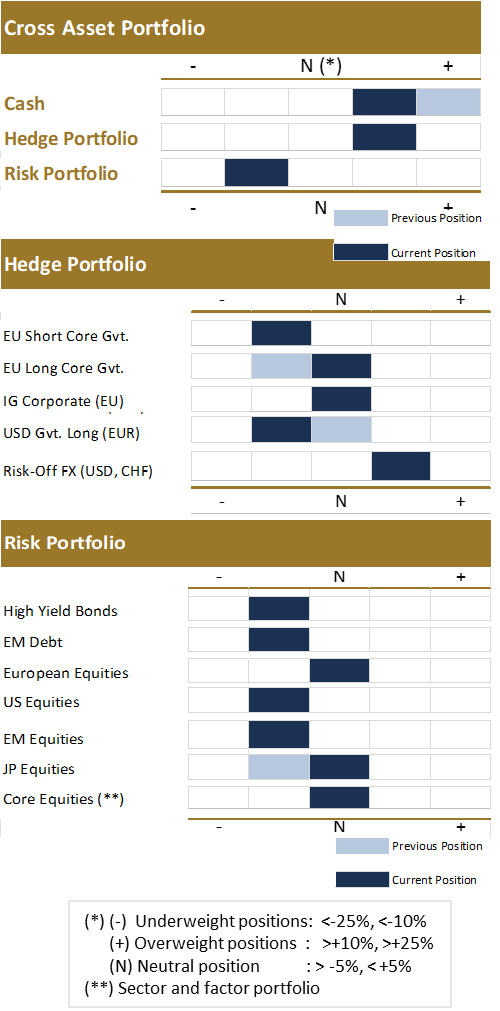

Our Risk Allocation Index continues to be modestly negative. It became negative in November due to negative inflation and business cycle signals. Hence, in our risk allocation, we underweight Risk assets at the start of 2022. At the same time, we overweight Cash/Hedge Assets.

Our global GDP model suggests that the global economy has slowed to around 3% by end-Q4. This is down from 5% at the start of Q3. According to our six mth. lead model, the slowing will continue in Q1 2022 to below 2.5%.

The global economy is slowing, but the path has been more a normalization than a real slow down. Hence, how fast and hard will the cooling become in H1 2022? The answers to this question are linked to both the inflation and the liquidity cycle:

Scenario 1: If inflation is getting out of control and sustainably high, funding rates will rise while cost inflation will squeeze profits and real incomes and slow the economy. As a result, the Liquidity cycle could, in this situation, weaken like in H2 2018

Scenario 2: If, on the other hand, inflation will cool off when short/medium-term supply-chain disruptions are resolved, the credit and liquidity cycle will stay positive together with profit margins and keep the global economy at a solid growth path despite the mature stage of the business cycle.

For now, we allocate with caution. That means that we follow the guidance of our Risk Allocation Index to reduce allocation to our Risk Portfolio. EMD, High Yield, and EM equities are unchanged in UW. We keep exposure to US stocks in UW. We stay Neutral in Core Equities & European Equities and upgrade Japanese stocks to Neutral from UW.

At the same time, we add to our Hedge & Cask portfolio, where we keep USD (& US 2Y rates) in OW together with Cash. We upgrade EU Long Core Gov.s from UW to Neutral. IG bonds are kept Neutral while the position in US Long bonds is reduced from Neutral to now UW.